Rental Criteria

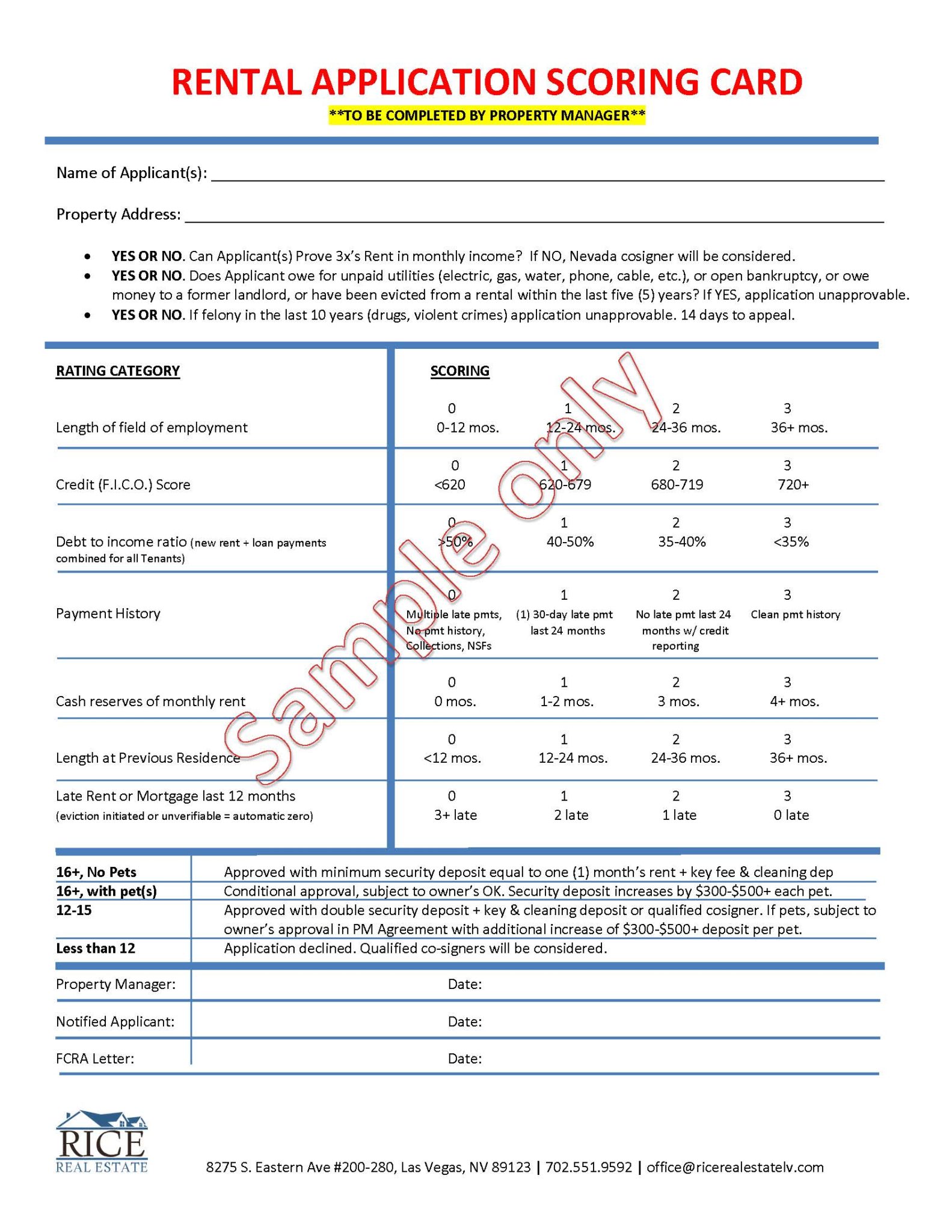

21 point scoring card

Rice Real Estate & Property Management’s rental criteria reference a 21-point scoring card, which can be viewed by scrolling down the page. The rental criteria scoring card is used to process and approve applications and is made accessible to all prospective applicants before applying for a rental home.

We score applications based on income, credit worthiness, debt to income ratio, rent payment history, cash reserves of monthly rent, employment history, length of residency, background/eviction check and other facts.

When a complete application is submitted our screening provider, TransUnion SmartMove, sends an email to the applicant asking them to release their personal information. This is standard for what is known as a soft credit check and does *not* require entering a social security number on Rice Real Estate & Property Management’s online application. This credit check will not affect the applicant’s credit history.

Tenant Screening *does* require the applicant’s involvement. This is beneficial as an applicant needs to confirm interest in the application process to complete this required step.

Income Requirements

2 Adults – at least 3xs rent

3 Adults – at least 4xs rent

4 Adults – at least 5xs rent

5 Adults – at least 6xs rent

and so on…

General Requirements

We use a rental application grading system that takes all aspects of the application into account. We process completed applications in the order received. A completed application means all supporting documents were received. If one application is incomplete, and another application comes in complete, we will process the completed application first. In the case of multiple applications, we reserve the right to accept the most qualified with respect to credit, rental history, income or employment history, and/or criminal history.

Each individual must complete and sign their own applications using their own separate email address – friends, family members, partners, and roommates must not send applications on behalf of others. We cannot process any application if we find evidence that it was submitted by another person.

False statements on any application = automatic decline.

Any application submitted using someone else’s personal information = automatic decline.

preview of rental application

Yes, it’s a lot of reading by today’s standards. Longer than a tweet, less fun than a text, not as interesting as a cat video on Facebook. But this is serious.

Thank you for considering a Rice Real Estate & Property Management managed rental home. We want your application and approval process to be easy so before you continue with the online application please take a few minutes and read the following important application information

- Application fee is $65 per applicant. The application fee can be paid online using an echeck or offline, in person, at our office (drop exact cash at 8275 S. Eastern Ave #200 Las Vegas 89123). Application fee is non-refundable.

- All applicants over the age of 18 must complete an application.

- Applicant should personally view the house both interior & exterior, prior to submitting an application.

- Documented monthly gross income must be at least 3x’s monthly rent. Self-employed & tip-earners included.

- If applicant currently owes for unpaid utilities, or owes money to a former landlord, or has been evicted from a rental within the last five (5) years the application will be declined.

- We only accept Nevada residents as co-signers. A co-signer must complete a separate rental application & will be required to execute the rental agreement along with the residents of the property. An approved co-signer will be fully obligated to all conditions and terms of the rental property lease. Automatic double security deposit if co-signer approved.

- Rice Real Estate reserves the right to process multiple applications. Rice Real Estate uses a 21-point scoring card to process applications. If multiple applications are received the property will be first offered to the applicant with the highest score. If the 1st approved applicant doesn’t pay holding fee within 24 hours of approval the property will be offered to the next in line and so on. The scoring card can be viewed here: Scoring Card

- Applicant understands Rice Real Estate incurs a cost processing applications and the $65 application fee is non-refundable.

- Once an application has been submitted and reviewed for completeness the applicant will receive a 3rd party email from SmartMove by TransUnion to approve running their credit/background/eviction check.

Here's what you'll need to have ready to apply

Have the following items ready to input data:

- Two (2) Previous Addresses and Landlord Information

- Employer: Name, Contact, Start Date, Salary

- Vehicles: make, model, color, year and license plate number

- Emergency Contact Information: Name, Phone, Relationship

- If applicable, photo of pet/animal and veterinarian records showing age, weight, breed, name and current shots

Have the following documents ready to upload:

- Copy of Government Issued Identification (i.e.- Drivers License, I.D. Card)

- Recent Paystub or Hire letter if starting new job

- Reliable documentation for other income you want included such as retirement, SSI, child support, etc.

- Most recent checking account bank statement. The statement must have applicant’s name visible and not be a screen shot of current balance. OK to black out account number.

- Recent savings account or retirement account showing cash reserves of monthly rent, if any.

- If Self-employed, 3 most recent business bank statements & last 2 yrs federal tax return with filing confirmation (IRS submission ID/ acknowledgment or you can contact the IRS to request a transcript for filed tax returns)

pets & animals

We require EVERYONE to complete a profile and review process to help ensure all of our residents understand our pet and animal-related policies (No Pet and Animal Policy | Pet Policy | Animal Policy). This process ensures we have formalized pet and animal-related policy acknowledgments and more accurate records to create greater mutual accountability. Review additional information about pets, pet deposits, and fees on our website.

Rice Real Estate & Property Management (RRE) is a pet-friendly management company. Our properties are owned by individual owners so certain properties may have further restrictions in addition to the standard pet policy. Individual owners may have additional restrictions above and beyond the FIDO score pricing notification. If you have more than two pets, or a special situation, please contact our office and we can provide additional guidance.

Please note that in the State of Nevada, landlord insurance companies can restrict coverage for animals with aggressive pasts or bite histories. In those scenarios, assume your application to rent will be denied without explicit approval in advance from the property owner or their insurance company

*We always accept emotional support and service animals with proper documentation. ESAs and service animals are not subject to any fees or deposits.

lease info & review sample lease

RENT PRORATION: All rents are prorated using a 30-day month. Leases that commence on or after the 15th day of the month will require the full payment of both the first month’s pro-rated rent and the full second month’s rent at the time of move-in.

PROPERTY RE-KEY: There is a $100.00 non-refundable rekey fee due at move-in. Tenant to schedule rekey upon possession.

SMOKING POLICY: All our rental properties are non-smoking properties. NO SMOKING or vaping of tobacco, herbal or other products is permitted inside any of our rental homes.

PET POLICY: All pets are subject to the property owner’s approval and Applicant must complete a profile for each pet. The security deposit will be increased by $300 or more (refundable) for each approved pet. A powerful breed pet such as a Pit Bull, Rottweiler, Doberman Pinscher, German Shepherd, Akita, Mastiff breeds, Chow Chow, American Staffordshire Terrier, powerful mixed breeds, etc., or any breed restricted by the homeowner’s insurance policy is not permitted. There is a $100+ one-time non-refundable pet fee per pet. There are additional monthly fees based on the pet’s FIDO pet score. View further information on our website page, which is dedicated to our pet policy.

RENTER’S INSURANCE: Applicant is required to purchase Renter’s Insurance. Before receiving keys, a copy of the Renter’s Insurance policy, listing the rented premise as the property insured, must be provided to the property manager. Rice Real Estate shall be listed on the policy as an additional interest. Renters with pet dogs must maintain a minimum $300,000 liability coverage. Renters of a pool property must maintain a minimum $500,000 liability coverage.

UTILITIES: Applicant is responsible to connect the following city utilities in applicant’s name: Electric, Gas, Water. The landlord will maintain the connection of the following utilities in the Landlord’s name: trash and sewer (separate sewer bill in Las Vegas only, not Henderson. In Henderson, the sewer utility is tied to the Tenant’s water bill). Other utility services may include satellite/cable access and telephone services, which are the sole responsibility of the Tenant.

NUMBER OF OCCUPANTS: Guideline for occupants allowed in the rental property is 2 people per bedroom, plus 1 extra person per property. Example: 1-bedroom rental = 3 people, 2-bedroom rental = 5 people, 3-bedroom rental = 7 peoples, etc.

FALSE INFORMATION: If any information provided on your application proves to be false or misleading, your application will be denied. If you have already entered a rental agreement on the property when it’s discovered you have provided false information, you will be subject to immediate eviction from the premises.

AGENCY DISCLOSURE: Rice Real Estate & Property Management is an agent for the property owner under separate management agreement. By submitting this application you acknowledge your understanding that our company represents the Owner(s) of the rental property. As Realtors, we will treat all parties to this transaction honestly, ethically and fairly.

FAIR HOUSING: Rice Real Estate & Property Management strictly abides by the Federal Fair Housing Act, Nevada Fair Housing Law and principles of Equal Opportunity. We do not discriminate based on race, color, religion, national origin, ancestry, sex, marital status, source of income, physical or mental disability, familial status, sexual orientation or gender identity/expression. Rice Real Estate & Property Management follows updated fair housing guidelines, including the Guidance on Application of the Fair Housing Act to the Screening of Applicants for Rental Housing published May 24, 2024.

ADDITIONAL LEASE INFORMATION: The lease admin fee of $100 is paid at move-in. Standard lease term is one (1) year. Rent must be paid in a single payment. Occupants will need to consolidate payments & submit ONLY (1) monthly rent payment. Rent posts on the 25th day of the previous month and is considered delinquent after the 1st. There is a grace period between the 25th of the month and the 1st. Rent will be considered late if paid on the 2nd of the month or later. There is a 5% late fee.

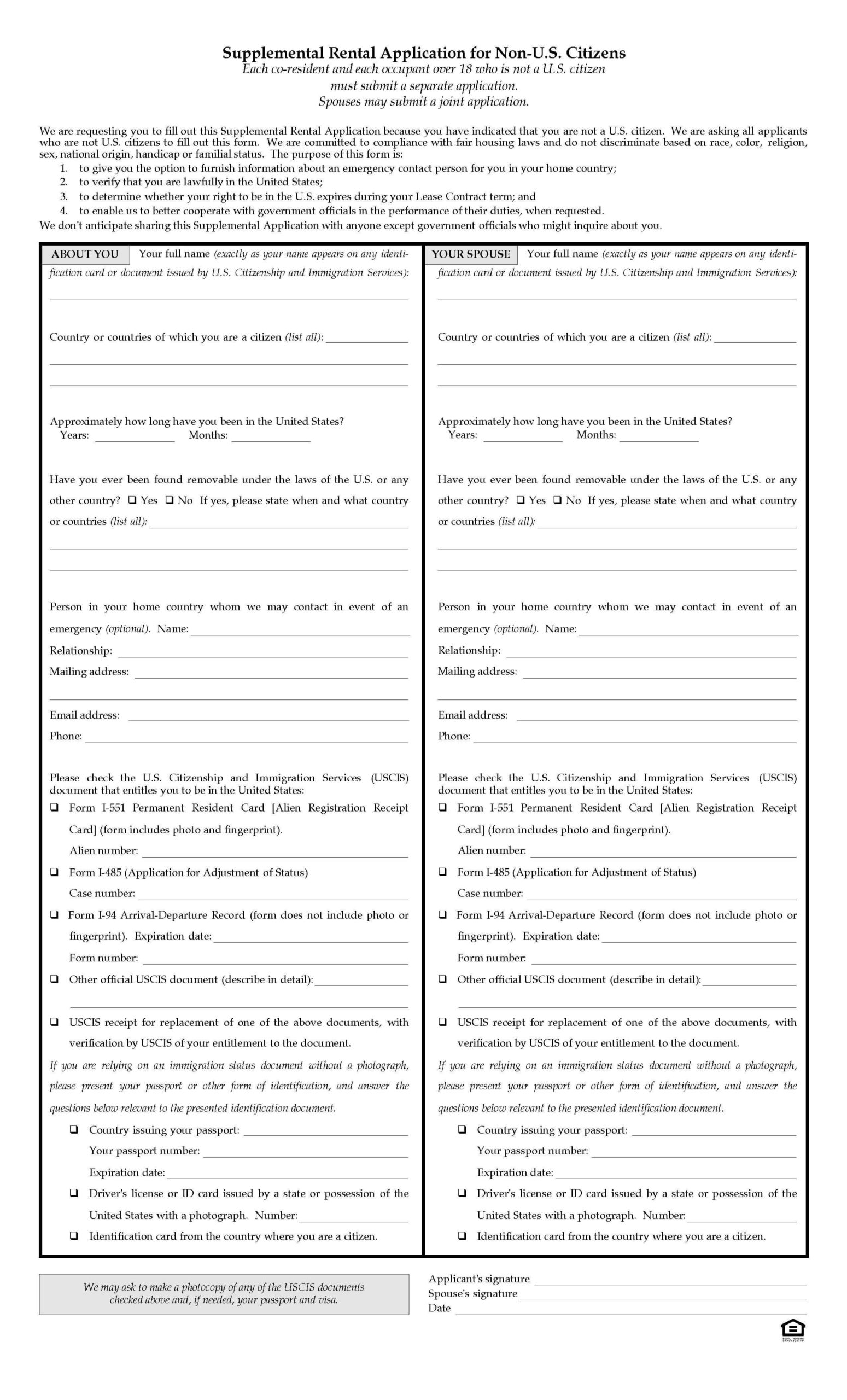

non U.S. citizen rental application addendum

Supplemental Rental Application for Non-U.S. Citizens: Each co-resident and each occupant over 18 who is not a U.S. citizen must submit a separate application.

adverse action letter

Should an application require double security deposit or be denied the applicant will receive an adverse action letter.

Date:

Dear Applicant:

Thank you for your recent rental application.

Action Taken

We regret that we are unable to approve your request at this time. Application declined.

We regret that we are unable to approve your request at this time under our standard terms

and conditions. We can, however, approve your rental application on the following terms*:

*If an offer is written above the offer is open for 48 hours, subject to the availability of the unit.

*If the offer is acceptable to you contact us.

Important Information.

We were unable to approve your application on the terms you requested for the following reason(s):

____ Application Incomplete

____ Unable to Verify Income 3x’s rent.

____ Currently owe unpaid utilities.

____ Currently owe money to a former landlord.

____ Prior eviction proceedings within the last 5 years.

____ Felony in the last 10 years (drugs, violent crime)

____ Temporary or Irregular Employment or Length of field of employment

____ False or Misleading Information on Application

____ Scoring Card less than 12 points. See attached scoring card.

____ Scoring Card 12-15 points. See attached scoring card.

____ Other

You credit score (as returned by TransUnion):

This score has a range of 300 to 850

In evaluating your application the consumer reporting agency(ies) listed below provided us with

information that in whole or in part influenced our decision. The reporting agency(ies) played no part in

our decision other than providing us with credit or criminal record information about you. Under the

Fair Credit Reporting Act, you have a right to know the information provided to us. It can be obtained by

contacting:

Credit Information

TransUnion LLC

Consumer Disclosure Center

P.O. Box 1000 Chester, PA 19022 (800) 888-4213

Rice Real Estate 8275 S. Eastern Ave #200-280 Las Vegas, NV 89123

Criminal or Eviction Information

(If “Prior Criminal History” or “Prior Eviction Proceedings” is checked above, the following

agency provided the criminal record information)

Vantage Data Solutions – 1-800-568-5665

You also have a right to a free copy of your report(s) from the reporting agency that provided the report,

if you request it no later than 60 days after you receive this notice. In addition, if you find that any

information contained in a report you receive is inaccurate or incomplete, you have the right to dispute

the matter with the reporting agency that provided the report or through RentPort consumer relations

at 1- 800-230-9376 or [email protected].

If you have any questions regarding this letter, you should contact us.

HUD Property Applicants: You have a right to respond to this letter by contacting us in writing

or requesting a meeting within 14 days to dispute this rejection. Persons with disabilities have

the right to request reasonable accommodations to participate in the informal hearing

process.

NOTICE: The federal Equal Credit Opportunity Act prohibits creditors from discriminating

against credit applicants on the basis of race, color, religion, national origin, sex, marital

status, age (with certain limited exceptions); because all or part of the applicant’s income

derives from any public assistance programs; or because the applicant has in good faith

exercised any right under the Consumer Credit Protection Act. The federal agency that

administers compliance with this law is the Federal Trade Commission, Equal Credit

Opportunity, Washington, D.C. 20580. 506485 (Ver. 8/01)

Para informacion en español, visite www.consumerfinance.gov/learnmore o escribe a la escribe a la Consumer Financial Protection Bureau, 1700 G Street N.W., Washington, DC 20006.

A SUMMARY OF YOUR RIGHTS UNDER THE FAIR CREDIT REPORTING ACT

The federal Fair Credit Reporting Act (FCRA) promotes the accuracy, fairness, and privacy of information in the files of consumer reporting agencies. There are many types of consumer reporting agencies, including credit bureaus and specialty agencies (such as agencies that sell information about check writing histories, medical records, and rental history records). Here is a summary of your major rights under the FCRA. For more information, including information about additional rights, go to www.consumerfinance.gov/learnmore or write to: Consumer Financial Protection Bureau, 1700 G. Street, N.W., Washington, D.C. 20006.

You must be told if information in your file has been used against you. Anyone who uses a credit report or another type of consumer report to deny your application for credit, insurance, or employment – or to take another adverse action against you – must tell you, and must give you the name, address, and phone number of the agency that provided the information.

You have the right to know what is in your file. You may request and obtain all the information about you in the files of a consumer reporting agency (your “file disclosure”). You will be required to provide proper identification, which may include your Social Security number. In many cases, the disclosure will be free. You are entitled to a free file disclosure if:

a person has taken adverse action against you because of information in your credit report;

you are the victim of identity theft and place a fraud alert in your file;

your file contains inaccurate information as a result of fraud;

you are on public assistance;

you are unemployed but expect to apply for employment within 60 days.

In addition, all consumers will be entitled to one free disclosure every 12 months upon request from each nationwide credit bureau and from nationwide specialty consumer reporting agencies. See www.consumerfinance.gov/learnmore for additional information.

You have the right to ask for a credit score. Credit scores are numerical summaries of your credit-worthiness based on information from credit bureaus. You may request a credit score from consumer reporting agencies that create scores or distribute scores used in residential real property loans, but you will have to pay for it. In some mortgage transactions, you will receive credit score information for free from the mortgage lender.

You have the right to dispute incomplete or inaccurate information. If you identify information in your file that is incomplete or inaccurate, and report it to the consumer reporting agency, the agency must investigate unless your dispute is frivolous. See www.consumerfinance.gov/learnmore for an explanation of dispute procedures.

Consumer reporting agencies must correct or delete inaccurate, incomplete, or unverifiable information. Inaccurate, incomplete or unverifiable information must be removed or corrected, usually within 30 days. However, a consumer agency may continue to report information it has verified as accurate.

Consumer reporting agencies may not report outdated negative information. In most cases, a consumer reporting agency may not report negative information that is more than seven years old, or bankruptcies that are more than 10 years old.

Access to your file is limited. A consumer reporting agency may provide information about you only to people with a valid need – usually to consider an application with a creditor, insurer, employer, landlord, or other business. The FCRA specifies those with a valid need for access.

You must give your consent for reports to be provided to employers. A consumer reporting agency may not give out information about you to your employer, or a potential employer, without your written consent given to

the employer. Written consent generally is not required in the trucking industry. For more information, go to

www.consumerfinance.gov/learnmore.

You may limit “prescreened” offers of credit and insurance you get based on information in your credit report. Unsolicited “prescreened” offers for credit and insurance must include a toll-free phone number you can call if you choose to remove your name and address from the lists these offers are based on. You may opt-out with the nationwide credit bureaus at 1-888-567-8688.

You have the right to place a “security freeze” on your credit report, which will prohibit a consumer reporting agency from releasing information in your credit report with your express authorization. The security freeze is designed to prevent credit, loans, and services from being approved in your name without your consent. However, you should be aware that using a security freeze to take control over who gets access to the personal and financial information in your credit report may delay, interfere with, or prohibit the timely approval of any subsequent request or applications you make regarding a new loan, credit, mortgage, or any other account involving the extension of credit.

As an alternative to a security freeze, you have the right to place an initial or extended fraud alert on your credit file at no cost. An initial fraud alert is a 1-year alert that is placed on a consumer’s credit file. Upon seeing a fraud alert display on a consumer’s credit file, a business is required to take steps to verify the consumer’s identity before extending new credit. If you are a victim of identity theft, you are entitled to an extended fraud alert, which is a fraud alert lasting 7 years

A security freeze does not apply to a person or entity, or its affiliates, or collection agencies acting on behalf of the person or entity, with which you have an existing account that requests information on your credit report for the purposes of reviewing or collecting the account. Reviewing the account includes activities related to account maintenance, monitoring, credit line increases, and account upgrades and enhancements.

You may seek damages from violators. If a consumer reporting agency, or, in some cases, a user of consumer reports or a furnisher of information to a consumer reporting agency violates the FCRA, you may be able to sue in state or federal court.

Identity theft victims and active duty military personnel have additional rights. For more information, visit www.consumerfinance.gov/learnmore.

States may enforce the FCRA, and many states have their own consumer reporting laws. In some cases, you may have more rights under state law. For more information, contact your state or local consumer protection agency or your state Attorney General. For information about your federal rights, contact:

TYPE OF BUSINESS:

PLEASE CONTACT:

1.a. Banks, savings associations, and credit unions with total assets of over $10 billion and their affiliates.

b. Such affiliates that are not banks, savings associations, or credit unions also should list, in addition to the Bureau.

a. Bureau of Consumer Financial Protection

1700 G Street NW

Washington, DC 20006

b. Federal Trade Commission: Consumer Response Center – FCRA

Washington, DC 20580

(877) 382-4357

2. To the extent not included in item 1 above:

a. National banks, federal savings associations, and federal branches and federal agencies of foreign banks

b. State member banks, branches and agencies of foreign banks (other than federal branches, federal agencies, and insured state branches of foreign banks), commercial lending companies owned or controlled by foreign banks, and organizations operating under section 25 or 25 A of the Federal Reserve Act

c. Nonmember Insured Banks, Insured State Branches of Foreign Banks, and insured state savings associations

d. Federal Credit Unions

a. Office of the Comptroller of the Currency

Customer Assistance Group

1301 McKinney Street, Suite 3450

Houston, TX 77010-9050

b. Federal Reserve Consumer Help Center

P.O. Box 1200

Minneapolis, MN 55480

c. FDIC Consumer Response Center

1100 Walnut Street, Box #11

Kansas City, MO 64106

d. National Credit Union Administration

Office of Consumer Protection (OCP)

Division of Consumer Compliance and Outreach (DCCO)

1775 Duke Street

Alexandria, VA 22314

TYPE OF BUSINESS:

PLEASE CONTACT:

3. Air carriers

Asst. General Counsel for Aviation Enforcement & Proceedings

Department of Transportation

400 Seventh Street SW

Washington, DC 20590

4. Creditors Subject to Surface Transportation Board

Office of Proceedings, Surface Transportation Board

Department of Transportation

1925 K Street NW

Washington, DC 20423

5. Creditors Subject to Packers and Stockyards Act

Nearest Packers and Stockyards Administration area supervisor

6. Small Business Investment Companies

Associate Deputy Administrator for Capital Access

United States Small Business Administration

409 Third Street, SW, 8th Floor

Washington, DC 20416

7. Brokers and Dealers

Securities and Exchange Commission

100 F St NE

Washington, DC 20549

8. Federal Land Banks, Federal Land Bank Associations, Federal Intermediate Credit Banks, and Production Credit Associations

Farm Credit Administration

1501 Farm Credit Drive

McLean, VA 22102-5090

9. Retailers, Finance Companies, and All Other Creditors Not Listed Above

FTC Regional Office for region in which the creditor operates or Federal Trade Commission: Consumer Response Center – FCRA

Washington, DC 20580

(877) 382-4357

The most advanced online Application.

Interested in applying for a home with Rice Real Estate & Property Management? Start the process online.